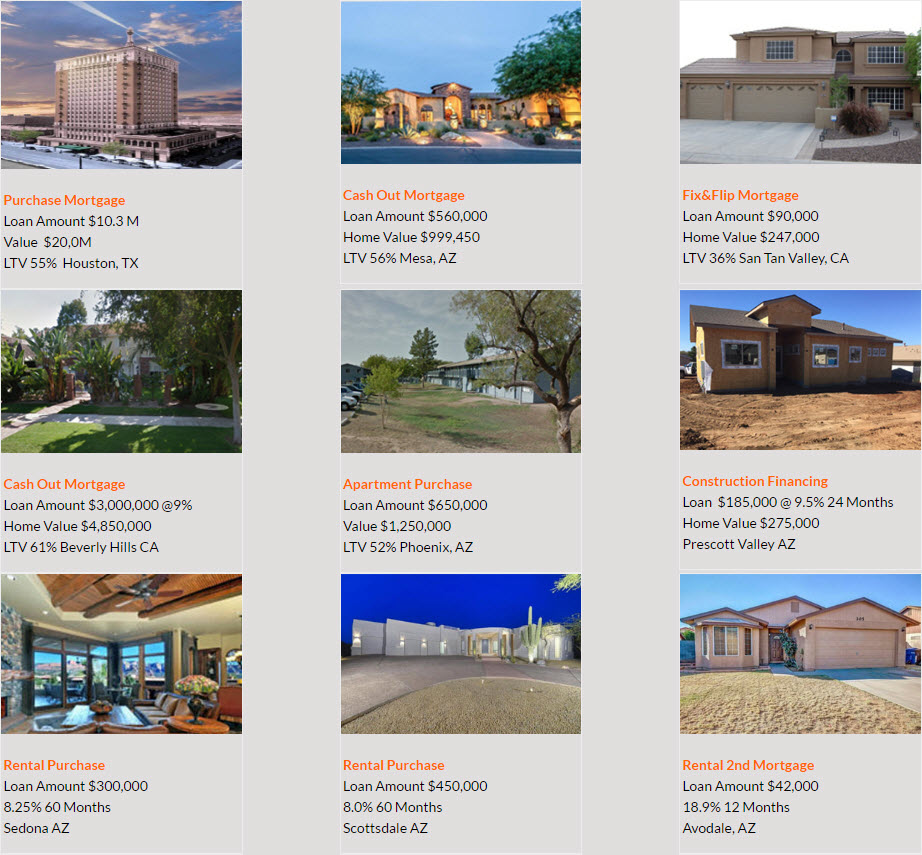

Commercial Lending - Private Hard Money Lenders

Loan Rates from 7.99% APR*

Investment - Fix&Flip - Bridge - Commercial - Business - Construction - Cash Out

• Fast/Easy Approval Process

• Loan Value Up to 90%*

• Funding in Days

• From $50,000 to $50,000,000*

• No Prepayment Penalties*

• PreApproved in 24 Hours

• Flexible Terms From 3 to 60 Months*

• Fixed Rate From 7.99% APR*

• Commercial/Construction Loans

• Business Loans/Fix&Fip Loans

• BBB A+ Rating

Latest News from the Blog

Considering a Commercial Hard Money Loan for your next commercial project or business plan?

If that’s where your financing search is headed important to

know the pros and cons of a commercial hard money loan.

By know you know California hard money loans are some of the most readily available hard money financing options, which is great for shopping around for the best rates and terms. But, in general, you may be wondering what exactly the benefits or rather advantages of California hard money loans are? Moreover, you may also want to know exactly what the disadvantages are of these particular kinds of loans. Well, the good news is the benefits outweigh the disadvantages by far.

Applying for a Commercial Bridge Loans

So you’ve decided that short-term financing is the best option for your new construction or upcoming investment. But, you’ve never applied for a commercial bridge loans before—no worries let’s go over the basics.

Applying for a commercial bridge loan is not necessarily any different than applying for any other kind of commercial loan. In other words, you still need the right documentation and a lender that understands your particular business needs or market. Thus, if this is not your first commercial loan, which it more than likely is not, you’re in luck. You do not have to lose sleep over narrowing down your short-term financing options.

With that being said, it may be more beneficial for you to focus on why a commercial bridge loans is right for you next project. For instance, say you already have an investment property or two underneath your belt and you are looking to make a few upgrades or improvements. If this scenario sounds familiar to you, then great! This is exactly the time for a short-term financing. Generally, you can be approved for this particular loan if your new construction will take some time but will not exceed three or more years depending on your specific market( hint: construction that takes longer than three years, in general, is not a little upgrade). In fact, non-residential bridge loans can be for a small time period of say two weeks or you if you go with a more traditional lender you may find bridge loans that range from 45 to 60 days.

Ultimately, when you start talking about years’ worth of upgrades you may want to rethink your need for short-term financing. However, it is important to note that you may be able to find a lender that offers what is known as bridge-to-permanent programs. These particular kinds of programs can make the transition from short-term financing to long-term financing more seamless (for a price of course.)

Applying for a Commercial Bridge Loans

So you’ve decided that short-term financing is the best option for your new construction or upcoming investment. But, you’ve never applied for a commercial bridge loans before—no worries let’s go over the basics.

Applying for a commercial bridge loan is not necessarily any different than applying for any other kind of commercial loan. In other words, you still need the right documentation and a lender that understands your particular business needs or market. Thus, if this is not your first commercial loan, which it more than likely is not, you’re in luck. You do not have to lose sleep over narrowing down your short-term financing options.

With that being said, it may be more beneficial for you to focus on why a commercial bridge loans is right for you next project. For instance, say you already have an investment property or two underneath your belt and you are looking to make a few upgrades or improvements. If this scenario sounds familiar to you, then great! This is exactly the time for a short-term financing. Generally, you can be approved for this particular loan if your new construction will take some time but will not exceed three or more years depending on your specific market( hint: construction that takes longer than three years, in general, is not a little upgrade). In fact, non-residential bridge loans can be for a small time period of say two weeks or you if you go with a more traditional lender you may find bridge loans that range from 45 to 60 days.

Ultimately, when you start talking about years’ worth of upgrades you may want to rethink your need for short-term financing. However, it is important to note that you may be able to find a lender that offers what is known as bridge-to-permanent programs. These particular kinds of programs can make the transition from short-term financing to long-term financing more seamless (for a price of course.)

Commercial Hard Money Lenders

Hard money loans lenders understand that even some of the most unlikely investment are still investments. So, if you thought there was no way you could quickly find financing for a foreclosure or another unlikely investment property with your credit think again!

Dealing with commercial lenders is never a walk in the park. But, with the right tools and clear plan you can easily navigate them. For instance, if you are dealing with commercial hard money lenders, then you may already know that there are lenders that often deal exclusively in one property type i.e. you will more than likely being dealing with niche lenders for hard money loans. Consequently, if you are actively looking for short-term commercial financing then it is clearly in the best interest of time to make sure that you are dealing with commercial hard money lenders in your particular market or property niche.

As previously suggested, hard money loans are ideal for such property types as foreclosures, land loan, construction loans, fix and flips, short sales, when you or your business need to move quickly and for when the potential buyer does not have the best credit or rather has certain credit issues. Moreover, lenders that typically offer these kinds of commercial loans are not banks. Thus, if you know ahead of time that you will not qualify for conventional financing, say yourself some time by not going through the lengthy process of applying for a bank loan.

So now that you know when to call on commercial hard money lenders and how to narrow down your potential list of lenders, let’s go over what to do if you are experiencing some difficulty actually finding a few good hard money lenders in your area and in your property niche.

Commercial Lending

Mortgages and Commercial Lending. If you got questions regarding your next commercial purchase, we’ve got answers.

The commercial real estate market is forever changing and if you do not take the time to keep up, you may be lost when it comes time to consider getting a commercial lending for your next endeavor. The truth is that more people than ever are creating new companies and running their own businesses. Moreover, many of these individuals have never had to borrow money for business—unless you’re counting student loans. But, all joking aside if this is your first-time “borrowing for business” you may be surprised at all the things you just didn’t know.

For starters, if you thought Fannie Mae or another governmental institution was going to be your new best friend think again. Though you can still count on these governmental mortgage institution for such commercial properties as multifamily housing, if you are not in the business of property management then you will more than likely not be dealing with old’ Fannie or Freddie. Thus, the majority of commercial lending loans are brought to you by banks, insurance companies and lenders (conduit, etc.).

So, now that you know just who you are dealing with, let’s talk about what happens next. Typically, before you reach out to a lender, bank or insurance company for financial assistance with your commercial venture, you should be clear on just how you are going to meet your future repayment terms and you should be clear on how much you actually need to borrow. These are important things to be clear on because your future commercial lending more than likely will be a nonrecourse loan i.e. the bank or lender can take the property in the event of a default (generally if you owe more than the value of the property at time of default, your other assets cannot be seized with a nonrecourse loan.).

Commercial Lenders – Know Your Eligibility

Before you consider a commercial mortgage, it is important to know what you need to qualify for one. Lender requirements are often just the beginning.

Commercial lenders i.e. non-residential mortgages are nothing to sneeze at. In other words, you’d be surprised how much of an impact commercial lenders have on the overall financial future of companies. Consequently, when it comes time to enter the vast world of non-residential mortgages, it is extremely important to your eligibility. Of course, you may be asking yourself, aren’t non-residential mortgages loans similar to most mortgage loans? Well, obviously the answer to that question is no.

In general, non-residential mortgages are viewed as high-risk loan for most lender, banks and insurance companies. Due to this industry fact, most lenders or banks have several requirements that a borrower must meet. Moreover, if a borrower is unable to meet all the requirement set out by the lender or bank then there simply is no commercial mortgage in that borrower’s future. At first glance, this may should a little harsh, but as previously mentioned these particular mortgages have a direct impact on the future of the company, which means the borrower’s ability to meet their repayment terms often rest on these requirements.

At this point, you may be fearful of your lender’s requirements for commercial lenders. But, you shouldn’t be. Your eligibility and your potential lender’s expectation do not have to be at odds if you know what you are up against.

Commercial Real Estate Lenders

Selecting the right lender for your commercial real estate lenders is never easy. But with a few key questions you can narrow down your options and ultimately choose the right lender for you.

Find the right lender for any commercial real estate loan is a big deal. It’s a big deal because these particular kinds of loans are truly not your everyday kind of loans. In other words, most lenders have ample experience in residential loans as everyone needs a home. But, of course, not everyone needs a business or an investment property and to each its own. Nevertheless, the point is that the majority of big lenders are better versed in all things residential. Therefore, it is your best interest to find a lender that has a substantial amount of experience with commercial real estate lenders.

Well, at this point, you may be wondering, just how exactly are you going find a lender that specializes or rather has the right amount of commercial loans underneath their belt? The trick is to ask the right questions. Asking the right questions may sound like a simple solution to ensure the future financial security of your company or business venture, but, the truth is it’s all in the details.

For instance, you may find a lender that has extensive experience with commercial real estate hard money lender, which is great. But, stop and ask yourself, does this lender know my market. In other words, your potential lender has extensive experience with commercial or rather non-residential loans, but in what market? You see details, they matter. Thus, with that being said, let’s go over a few more key questions that will help you find the right lender for you and your specific market.

What Commercial Lending Real Estate Loans Are Right For You?

Everyone expects to need a commercial lenders when they open a business, but do they know what kind to get? Knowing the types of loans available can be helpful to know as you get started and just in case something happens.

Deciding you want to go into business for yourself is a pretty big deal. No longer will you have to answer to the beck and call of a superior. You will be the superior that everyone else answers to, brings problems to, and expects to have all the answers.

Not only will you need to have all the answers, but you will need to have money. Getting a business off the ground takes money; money that most people will get through commercial lending from their bank.

Yes, there are different types of loans.

Understanding the Different Types of Commercial Real Estate Loans

There are different types of loans you can apply for through your bank. Each has various aspects that are necessary to know and understand:

Bridge Loans are short term loans borrowers can apply for when they need cash right now to cover expenses. They are typically short-term loans through private lenders who will require proof of income and an excellent credit score.

Real Estate Purchase Loans are the loans you take out to purchase your building, store, or office. These can come with fixed or adjustable rates, will require the borrower to have excellent credit and significant savings in a business and personal account. The commercial property itself will need to be used as collateral.

Hard Money Loans are for when an infusion of cash is needed sooner rather than later, often to save the business or keep it afloat. Since they are given when a business is in dire need, they often come with a higher interest rate to compensate the lender for taking on greater risk.

Joint Venture Loan are what want if you are going into business with a partner. They are common when neither party can receive approval on their own but by applying together, they can make a better case to the lender.

Participating Mortgage is a type of loan gives the lender a chance to enjoy the success of the business. When payments are due, the borrower will send a percentage of the income earned as well as payment. This kind of relationship is more common between lenders and long-term, financially stable borrowers.

How Does Knowing the Different Type Of Commercial Real Estate Loans Help You?

When you go into business, you will have a plan, and a few contingency plans to help you deal with whatever problems or issues that may arise. More often than not, challenges and problems will require some sort of financial commitment.

If you have the cash on hand—great, but if not, it can be nice to know there are different types of commercial lenders that may help you.